California, often considered a trendsetter for global policies, has recently enacted two significant climate laws: The Climate Corporate Data Accountability Act (SB 253) and The Climate-Related Financial Risk Act (SB 261), reflecting the state’s influential role in driving national and global change. These laws, passed in 2023, underscore California’s commitment to addressing the urgent risks posed by climate change.

Now, thousands of organizations operating in California are mandated to provide carbon emissions data, including scope 3 emissions throughout their value chains. This shift from voluntary to mandatory reporting marks a significant milestone, prompting businesses to implement changes to comply with emerging regulations and prioritize climate action. Strong climate reporting capabilities, including audit-ready carbon accounting, are becoming essential for corporate leaders to navigate not only California’s requirements but also similar regulations emerging worldwide.

SB 253: Climate Corporate Data Accountability Act

The California legislature recently passed SB 253, aimed at providing stakeholders such as investors, consumers, and communities with transparent information about the sources of carbon pollution from companies operating in the state. This development reflects a broader global trend toward advancing climate-related disclosure regulations. Despite an initial failed attempt, a revised version of SB 253 passed with significant support, driven by the demand for standardized climate-related disclosures and endorsement from major companies such as Apple, Adobe, Microsoft, etc. Unlike its predecessor, the revised SB 253 includes provisions to ease the reporting burden on entities, such as introducing a phase-in period for verifying greenhouse gas (GHG) emissions data and imposing an annual filing fee payable to the California Air Resources Board (CARB) to assist in enforcing reporting requirements.

1. Criteria for Coverage under SB 253

SB 253 applies to both public and private companies organized in the United States with annual revenues exceeding $1 billion that are doing business in California. While the bill is silent, it will most likely be up to the CARB to determine how the $1 billion threshold is calculated, including whether it includes the revenues of all affiliates and subsidiaries, and whether it includes global or only domestic revenues.

The phrase “doing business in California” is interpreted as “actively engaging in any transaction for the purpose of financial or pecuniary gain or profit.” An entity is considered to be conducting business in California for a given tax year if it meets any of the following conditions:

The company is either organized or commercially domiciled in California.

Sales made by the company in California during the tax year exceed either $500,000 or 25% of the company’s total sales, whichever is lower.

The value of the company’s real property and tangible personal property in California is greater than either $50,000 or 25% of the company’s total real property and tangible personal property, whichever is lower.

The amount the company pays in compensation in California exceeds either $50,000 or 25% of the total compensation paid by the company, whichever is lower.

2. Implementation Timeline and Required Disclosure

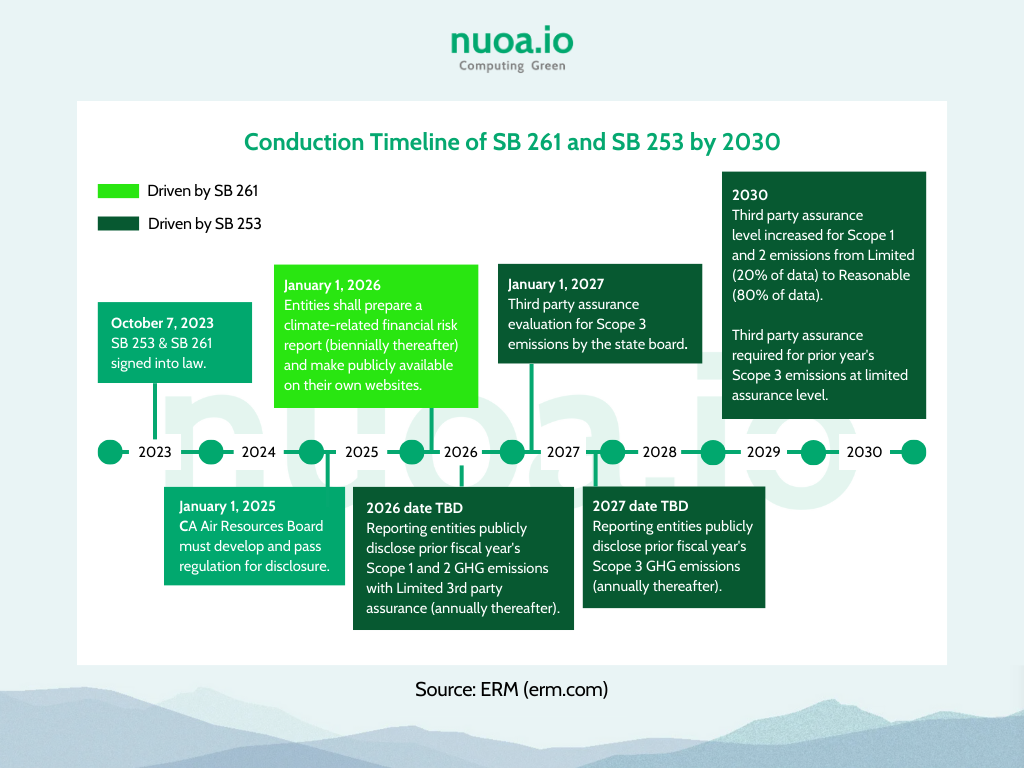

The reporting obligations begin in 2026, with CARB tasked by the Legislature to establish a regulatory framework by January 1, 2025.

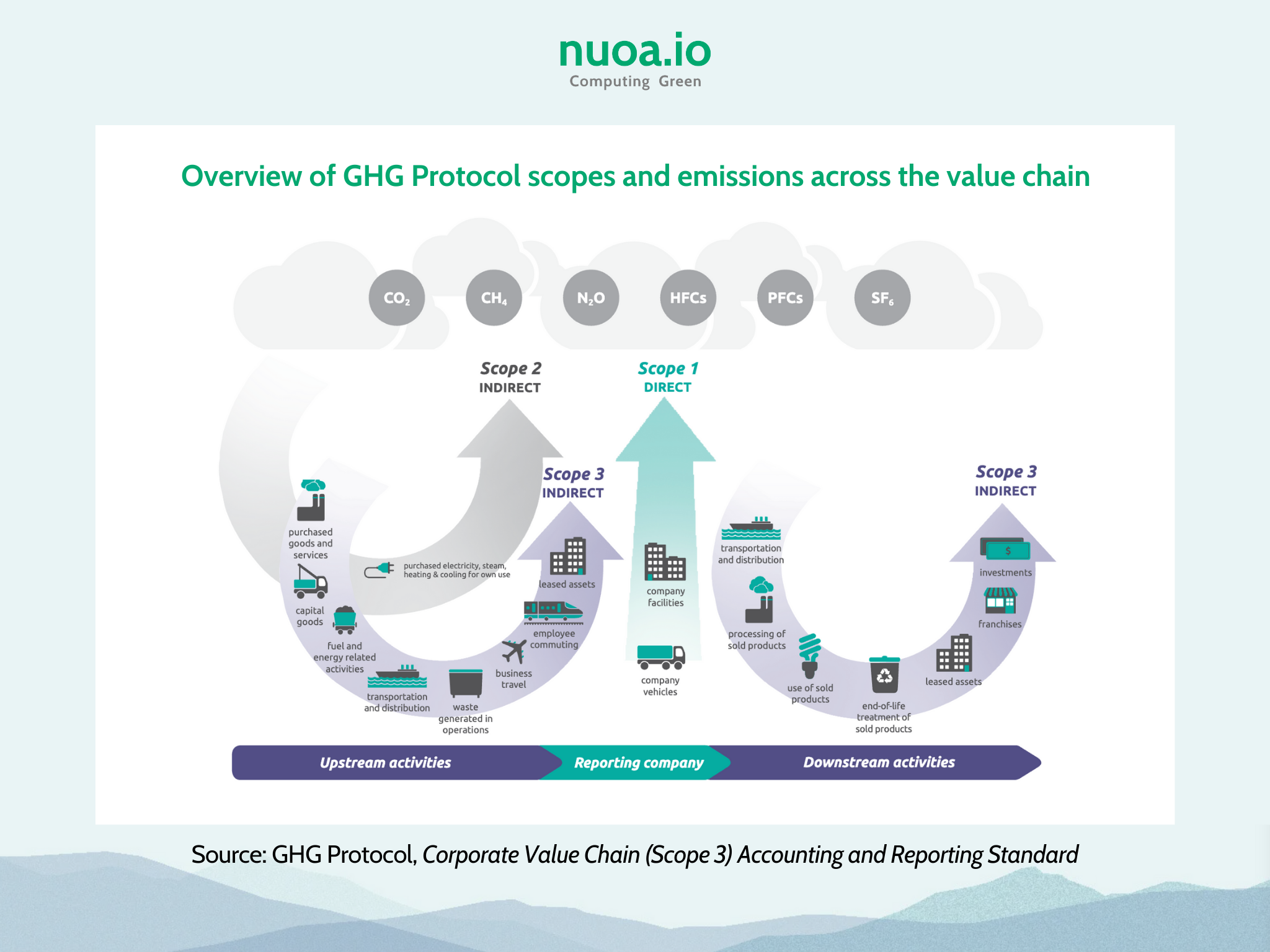

SB 253 adopts the “scope” framework from the 2001 World Resources Institute and World Business Council for Sustainable Development.

Scope 1: Direct emissions from sources owned or controlled by the reporting entity.

Scope 2: Indirect emissions resulting from purchased electricity, heating, or cooling.

Scope 3: This encompasses all other indirect emissions in a company’s supply chain.

Initially, only reporting for Scope 1 and 2 emissions will be enforced in 2026, with Scope 3 reporting starting in 2027. CARB will review and possibly adjust disclosure deadlines in 2029, considering input from industry stakeholders and avoiding redundancy with other emissions reports.

Furthermore, SB 253 mandates emissions calculations to adhere to the GHG Protocol standards and related guidance, including the Greenhouse Gas Protocol Corporate Accounting and Reporting Standard. The disclosed emissions data will be made publicly available through a digital platform managed by the selected nonprofit organization. Additionally, the CARB will collaborate with academic institutions to prepare an annual report on emissions data.

3. Enforcement Measures

SB 253 mandates that companies’ disclosures undergo third-party audits. Initially, the audit requires a “limited assurance” level, which essentially means that no errors or misstatements were found. However, starting in 2030, audits for Scope 1 and 2 emissions must meet a stricter “reasonable assurance” threshold, where the auditor must concur with the conclusion. Scope 3 emissions have a more relaxed requirement, needing only a reasonable basis and good faith disclosure. For violations, administrative penalties cannot exceed $500,000 per reporting year. CARB will take into account relevant factors, such as an organization’s compliance history and efforts to comply, when determining penalties. It’s important to note that the enrolled bill does not provide a private right of action. Enforcement is expected to be handled by CARB or referred to the California Department of Justice.

SB 261: Climate-related Financial Risk Act

SB 261, passed one day following SB 253, mandates that eligible companies must release biennial climate risk reports in a manner similar to the Task Force on Climate-related Financial Disclosures (TCFD) guidelines. Additionally, the legislation tasks CARB with contracting a climate reporting organization to assess and scrutinize these reports, highlighting any deficiencies or incompleteness in the disclosures.

1. Criteria for Covered Companies under SB 261

SB 261 applies to both public and private companies operating in the United States with annual revenues exceeding $500 million if they conduct business in California. However, entities regulated by the California Department of Insurance or involved in the insurance industry in any state are exempt. This legislation encompasses around 10,000 companies in California with revenues exceeding $500 million annually, excluding insurance firms, which are already overseen by the state’s Department of Insurance for climate-related risks.

2. Implementation Timeline and Required Disclosure

Covered companies are required to publish their initial risk reports by January 1, 2026, and then subsequently every two years thereafter. Similarly, the climate reporting organization must also produce its public report biennially.

Every two years, covered entities are obligated to produce a climate-related financial risk, which is defined as a “material risk of harm to immediate and long-term financial outcomes due to physical and transition risks, including, but not limited to, risks to corporate operations, provisions of goods and services, supply chains, employee health and safety,” and more report following the guidelines outlined in the Final Report of Recommendations from the TCFD. This report should address the risks posed by climate change to both immediate and long-term financial outcomes, encompassing a wide range of factors such as corporate operations, supply chains, employee well-being, investments, and overall economic stability.

The SB 261 will soon officially take effect on entities it mandates, starting from January 2026

The specific requirements for disclosure are still evolving, with SB 261 tasking CARB with engaging a nonprofit climate reporting organization to develop best practices for reporting financial risks related to climate change. Entities must strive to complete their disclosure to the best of their ability, providing detailed explanations for any gaps in reporting and outlining steps to achieve comprehensive disclosure. Additionally, compliance with other reporting frameworks may fulfill the requirements of SB 261.

3. Enforcement Measures

SB 261 mandates that CARB establish regulations enabling the imposition of administrative penalties for failure to file, late filing, or other reporting-related deficiencies. These fines are limited to $50,000 per reporting year, a substantial reduction from the previous cap of $500,000, as initially proposed similar to California SB 253.

Preparing For SB 253 and SB 261

To prepare for SB 253, businesses must prioritize the collection of emissions data, commencing in 2025 to meet the reporting deadlines set for 2026. This transition demands the same level of careful attention applied to financial data, necessitating robust internal controls. Moving from voluntary to regulated reporting requires heightened examination of emissions data, akin to financial data, with rigorous internal review and third-party assurance becoming standard practice. To navigate this shift effectively, companies must ensure transparency and accuracy in their data, relying on technology for automated carbon accounting to guarantee traceability and reliability.

Challenges in Implementation

These bills will need to weather two major challenges as they face funding delays and legal opposition in their implementation journey.

Governor Newsom has paused funding for SB 253 and SB 261, along with other state laws, until May 2024 due to a projected budget shortfall of nearly $38 billion. Despite CARB’s need for approximately $9 million to implement the legislation, funding remains on hold.

Major business groups, such as the US Chamber of Commerce and the American Farm Bureau Federation, have initiated legal proceedings against California’s climate laws, asserting multiple constitutional and legal arguments. Firstly, they contend that these laws violate the First Amendment by compelling companies to express views they consider controversial, without a clear commercial purpose. Additionally, they argue that SB 253’s requirement to disclose emissions beyond California’s borders conflicts with federal law, particularly the Clean Air Act, which they assert governs such matters exclusively at the federal level. Moreover, the lawsuit alleges that SB 253 and SB 261 overstep constitutional boundaries by attempting to regulate extraterritorial activities, which they argue falls outside California’s jurisdiction and could infringe upon interstate commerce protections.

Despite these challenges, CARB is expected to proceed with implementation, albeit potentially facing delays. Such a wait-and-see approach carries its own risks, particularly given the looming reporting deadlines starting in January 2025. In the meantime, businesses should focus on establishing robust governance structures and data collection processes to navigate not only the requirements of these laws but also the evolving landscape of sustainability-related regulations worldwide.

Conclusion

California’s climate disclosure laws, SB 253 and SB 261, represent significant steps toward addressing the urgent risks posed by climate change and driving corporate accountability. Despite facing challenges, these laws underscore the state’s commitment to climate action and serve as crucial tools for promoting transparency and sustainability in business operations. As organizations navigate the implementation process, prioritizing data collection, governance, and compliance with emerging regulations will be essential to meet reporting requirements and contribute to global efforts in combating climate change.

Lead Author:

Hieu Dinh Founder, CEO Email: hieu.dinh@nuoa.io

Co-Author: Linh Tran Business Analyst – Nuoa.io Email: linh.tran@nuoa.io