In 2020, while stuck in the United States due to the COVID-19 pandemic, I was “astounded” by the success of the Vietnamese government in controlling the outbreak domestically and maintaining economic growth. A bright spot came from one of the five key export sectors of our country, the textile and garment industry, when Vietnam surpassed Bangladesh to become the world’s second-largest exporter of textiles and garments, according to 2020 statistics from the World Trade Organization (WTO) [1].

However, from late 2022 to the end of the first quarter of 2023, many textile and garment enterprises had to scale back production and lay off thousands of workers due to a sharp decline in export orders [2]. Pouyen, the textile and garment enterprise that hires the most workers in Vietnam, announced the dismissal of nearly 6,000 employees [3]. According to the General Statistics Office, the export turnover of the textile and garment industry in the first quarter of 2023 decreased by nearly 20% compared to the same period. The Vietnam Textile and Apparel Association (VITAS) has assessed that the difficulties stem from various factors, including the impact of the conflict in Ukraine, global inflation, along with the aftermath of COVID, leading to a decrease in global purchasing power [4].

However, the global challenges mentioned by VITAS do not have a significant impact on Bangladesh, a direct competitor to Vietnam. From mid-2022 to the first quarter of 2023, not only did Bangladesh reclaim its second-place position in the world from Vietnam, but its textile and garment industry also experienced significant growth. Their export turnover increased by 14% in their main market, Europe, and by 35% in other non-traditional markets, according to the Export Promotion Bureau (EPB) of the Ministry of Commerce of Bangladesh [5].

Before diving into the analysis, I want to cite the export turnover figures of the textile and garment sector of both Bangladesh and Vietnam and compare them over two time periods:

Annual statistical data over the past 23 years, from 2000 to 2022.

Monthly report data for the latest 22 months, from July 2021, after the pandemic was effectively controlled in both countries.

Chart 1: A comparison chart of the annual total export turnover of the textile and garment sector between Bangladesh and Vietnam, based on data from 2000 to 2022, compiled by the author from the World Trade Organization (WTO), the Bangladesh Garment Manufacturers and Exporters Association (BGMEA), and the General Statistics Office of Vietnam (GSO) [6].

Taking a comprehensive look at the data from 2000 to the present, Vietnam has consistently trailed behind Bangladesh in terms of the value of textile and garment exports (see Chart 1 alongside). In 2020, which was the only year we surpassed Bangladesh, the difference was very small, with just over $500 million in export value. Starting from 2021, Bangladesh quickly recovered production and experienced growth at a much faster pace than in previous years, with the total export turnover in 2022 increasing by nearly 30% compared to the previous year.

When we examine the monthly data more closely from mid-2021 to the present, Bangladesh has shown stable growth in total export turnover. Although there were slight declines in March and April of this year compared to the same period, due to the Eid al-Fitr holiday marking the end of the Ramadan fasting month for Muslims, Bangladesh quickly bounced back with export values surpassing $4 billion, a 28% increase compared to the same period last year.

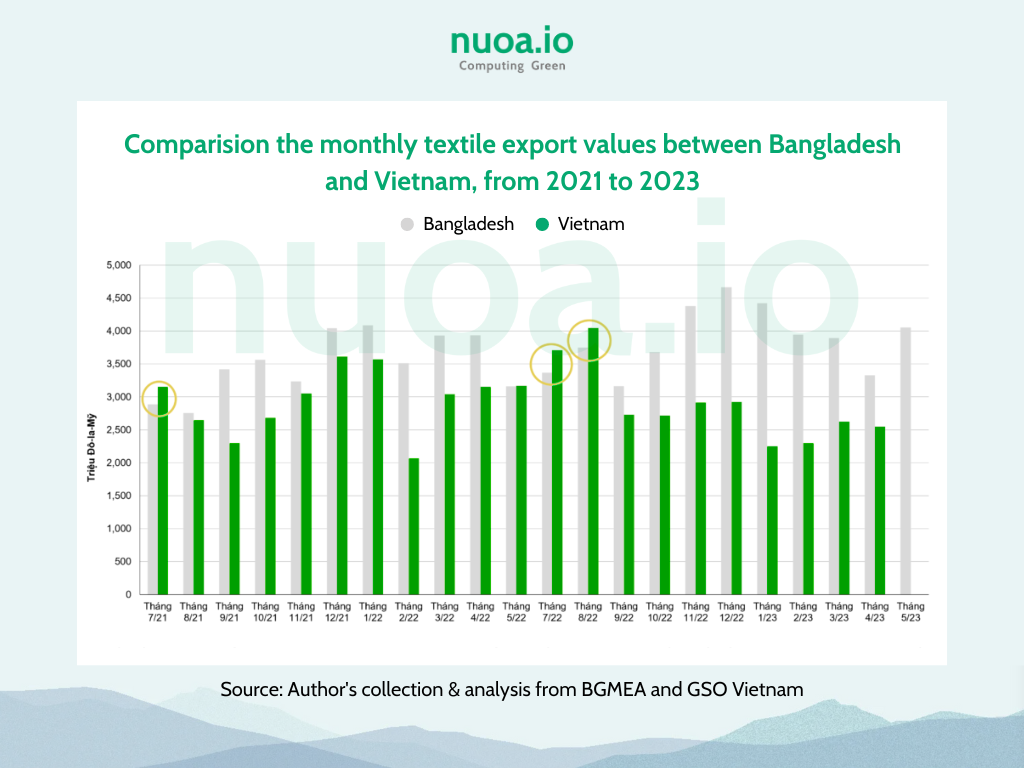

When compared to our country, Bangladesh consistently has higher export values than Vietnam, with a significant difference (nearly double) in the last four months of 2022 and the beginning of 2023, and only lower than our country at three points: July 2021, July 2022, and August 2022 (see Chart 2 below).

Furthermore, the bleak picture of Vietnam’s textile and garment industry becomes even more pronounced, especially from September 2022, when export turnover began to sharply decline, with five months of negative growth compared to the same period last year from October 2023 to date (May data not yet disclosed).

Chart 2: A comparison chart of monthly export turnover of the textile and garment sector between Bangladesh and Vietnam, based on data from July 2021 to May 2023, compiled by the author from the World Trade Organization (WTO), the Bangladesh Garment Manufacturers and Exporters Association (BGMEA), and the General Statistics Office of Vietnam (GSO) [6].

My research and that of my colleagues at Nuoa.io indicate that there are specific reasons leading to the contrasting picture between the textile and garment industries of Bangladesh and Vietnam from 2022 to the present.

Firstly, Vietnam is facing specific challenges with its primary export market being the United States. “The Uyghur Forced Labor Prevention Act (UFLPA)” passed in 2021 requires the prohibition of importing goods originating from Xinjiang, China [7]. According to the U.S. Customs and Border Protection (US CBP) in early May 2023, over $2 million worth of textile and footwear shipments from Vietnam were denied entry. More than $10 million worth of shipments are awaiting inspection based on new import standards under the UFLPA law [8].

While the number may not be substantial, the garment orders delayed entry into the U.S. due to the UFLPA law primarily originate from Vietnam. Our country primarily imports cotton from China, and over 90% of the cotton produced in China comes from Xinjiang, according to the Observatory of Economic Complexity (OEC). Meanwhile, Bangladesh primarily imports cotton from India and does not encounter this issue. Vietnam’s textile and garment industry may have faced “unforeseen losses” from the U.S.-China political standoff.

Secondly, not only does Bangladesh dominate the basic apparel segment with lower-than-average world prices at the port of export (FOB prices) due to the advantage of cheap labor, but it has also expanded its supply to sustainable apparel markets with higher value-added [9]. Thanks to early investment in green production, the textile and garment industry in this country is ahead of the increasing trend of green consumption worldwide.

In the two most recent surveys in 2021 and 2020 on consumption trends in Europe, 33% of consumers in Poland and 38% of consumers in the UK and Germany, when asked, stated that “reducing environmental impact” is one of the top three most important criteria when deciding to purchase clothing, according to reports from Vogue magazine and Boston Consulting Group, and research by McKinsey & Co. [10,11].

Even in the United States, the traditional market for Vietnamese apparel, 19% of consumers, mostly those under 40 years old, are willing to pay a higher price for products with less environmental impact, according to a 2019 study by McKinsey & Co. [12]. These surveys all indicate that environmentally friendly products are becoming an expectation rather than an exception for consumers, especially for the Gen Z generation (born from 1997 to 2012) and Millennials (born from 1981 to 1996).

The “decarbonize” revolution in Bangladesh’s textile and garment industry over the past decade has excellently kept pace with this global consumer trend. The top 20 largest exporting companies in Bangladesh all have manufacturing plants certified with “Leadership in Energy and Environmental Design” (LEED) certification, awarded by the U.S. Green Building Council (USGBC). [13].

From 2016 to early 2023, Bangladesh has seen the number of green factories certified with LEED certification increase from 36 to 196. [13]. These green factories are capable of reducing energy consumption by 40% and water consumption by over 30%, contributing significantly to a large reduction in greenhouse gas (GHG) emissions directly from the production process, according to statistics from the Bangladesh Garment Manufacturers and Exporters Association (BGMEA) and a study from the University of California, Berkeley, USA. [14]. Therefore, Bangladesh can easily meet the stringent environmental standards of the growing sustainable apparel market.

The strong spread of green consumer trends worldwide is leading to increasingly elevated policy barriers such as tariffs. In early 2023, two environmental policies related to greenhouse gas emissions were passed by the EU as part of the European Green Deal.[15]. The first is the Carbon Border Adjustment Mechanism (CBAM), under which the EU will impose taxes on goods exported to this market, based on the intensity of greenhouse gas emissions in the production process in the exporting country. [16]. Alongside that, the Corporate Sustainability Reporting Directive (CSRD) requires over 50,000 listed EU companies to report environmental impacts and social responsibilities starting from 2024. [17]. Therefore, these businesses have all planned to reduce GHG emissions across the supply chain to avoid exceeding the allowable emissions limit. This will have a significant impact on large exporting businesses to the EU market in the near future.

Based on the lessons learned from Bangladesh and considering the rapid changes in consumer behavior and environmental policies from the EU market in particular and the world in general, as well as avoiding being drawn into increasing trade tensions between the US and China, I believe that Vietnam’s textile and garment industry not only needs to seek new sources of raw materials but also urgently needs to transition towards green and sustainable production.

It will require many synchronized solutions to revive the textile and garment industry, but considering the green consumer trend, I, along with the research team on environmental solutions at Nuoa.io, propose three solutions for Vietnam’s textile and garment industry to align with green production and regain growth.

1. Directly reduce GHG emissions from production activities.

The first solution aims to directly reduce greenhouse gas emissions from production activities. Saving energy from equipment related to heating, ventilation, and air conditioning systems, along with gradually phasing out coal for electricity generation in the fabric dyeing process, are easily implementable solutions that also save production costs. Businesses can start implementing new technological solutions in the production process, such as waterless dyeing, to reduce energy consumption and contribute to reducing direct emissions from factories. [18]. Energy saving also plays a crucial role in the current context of local power shortages. [19].

2. Transitioning to the use of renewable electricity to indirectly reduce greenhouse gas emissions.

The second solution involves transitioning to the use of renewable electricity to indirectly reduce indirect greenhouse gas emissions related to purchasing electricity. In Vietnam, this solution has been successfully implemented by Hansoll Textile, a South Korean textile company supplying global brands such as Uniqlo, Gap, Target, and Walmart, and owning a chain of factories located in Vietnam. Hansoll has been using nearly 20% of its annual electricity consumption from rooftop solar power at 2 factories in southern Vietnam. According to research from the World Resources Institute (WRI), Hansoll estimated to have saved 3.75 billion dong in costs in the first year of operation. [20]. This story is a clear example demonstrating that the potential for transitioning to the use of renewable electricity in Vietnam is significant.

3. Implementing calculation and baseline measurement of GHG emissions.

The third solution, which is essential as it serves as a foundation for the two solution groups mentioned above and incurs minimal costs, is to promptly initiate the calculation and measurement of baseline greenhouse gas emissions. With the goal of accessing the sustainable apparel segment to diversify export markets and increase value, domestic enterprises need to promptly conduct greenhouse gas emissions inventories to serve sustainability reporting and develop optimal strategies for reducing greenhouse gas emissions. Indeed, only then can we meet stricter export standards and avoid being affected by policy barriers such as carbon export taxes from the EU.

Investing in green production and reducing emissions is an opportunity for our textile industry to catch up with the green consumer trend, achieve more sustainable growth amidst global economic fluctuations, and continue to provide employment for millions of workers nationwide!

Tác giả chính

Nguyễn Ngọc Lan Co-Founder, Giám đốc Khoa học & Chính sách Email: lan.nguyen@nuoa.io

Ms. Lan Nguyen does her PhD research in Economics, Environment, Evolution, and Ecology at the prestigious Dartmouth College (USA). Her research focuses on green growth policy, natural resource management, and environment policy and ecology.